Disability Insurance: An Overlooked Necessity

Darby Affeldt, DVM, North Star Resource Group, Seattle, Washington

Veterinarians agree on the importance of vaccinating patients to prevent future infections. Most have likely treated dogs and cats not properly protected by vaccination and thought, What a shame—this could have been prevented.

They should apply the same logic to income protection—and seek out quality disability insurance to prevent future loss of income. Unfortunately, just as clients do not always follow recommendations to vaccinate their pets against infectious diseases, veterinarians tend to ignore the need for disability insurance.

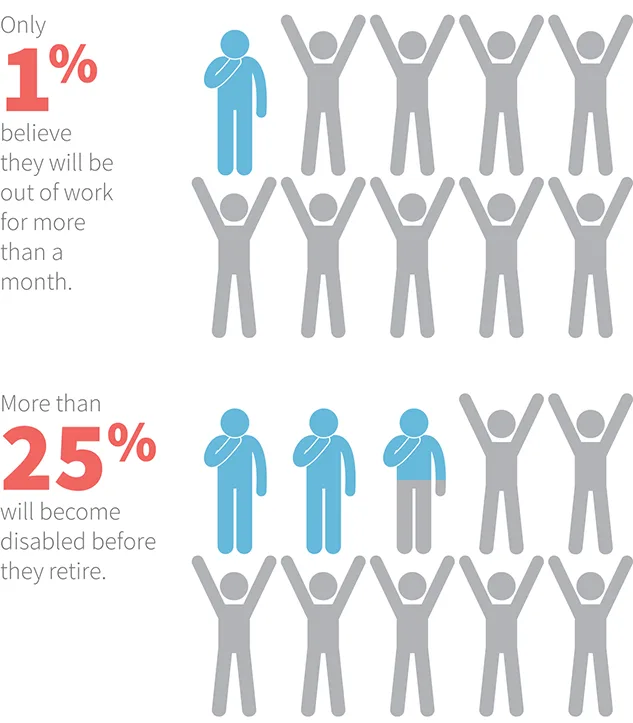

Figure 1 Many veterinarians ignore the need for insurance despite data that show high disability rates. Source: Council for Disability Awareness

Sadly, disabilities are not uncommon. Slightly more than 1 in 4 of today’s 20-year-olds will become disabled before they retire,1 and every 7 seconds, someone in the US suffers an injury or illness that will prevent him or her from working for at least a month, with the average disability absence lasting about 2.5 years.2 (See Figure 1, Figure 2 & Figure 3.)

The fact that disability insurance products are deeply complicated cannot be emphasized enough. Not all disability policies are the same, understanding the fine print is critical, and seeking advice from a licensed, trained, independent financial professional is paramount. Policies should also be checked annually to ensure the correct amount of income is being protected.

Own Occupation Policies

Designing a policy to fit an individual is similar to formulating treatment plans for each patient—the details matter. Veterinarians should pay close attention to the Definition of Occupation and be sure to seek policies that are occupation-specific throughout the life of the policy. True Own Occupation policies will pay the total disability benefit if a disabling injury or illness prevents a veterinarian from performing the material and substantial duties of his or her Own Occupation (ie, the specific duties being performed at the time of claim), even if the veterinarian chooses to work in another occupation while disabled.

By contrast, Modified Own Occupation or Any Occupation policies may pay less or stop paying benefits completely if the veterinarian chooses to work in the veterinary industry in a different capacity (eg, lecturing) or in a completely different occupation.

Riders

Attention should also be paid to the need for extra options, called riders. Insurance policies usually replace 60% to 70% of income, but various riders—some included in the base premium, some costing extra—are available. One example is the Cost of Living Adjustment (COLA), which increases the amount of benefit annually to keep pace with inflation. Without a COLA rider, a policy secured in 2016 to protect $4000 of income per month would provide the equivalent of $1647 per month in 2046 at an annual 3% rate of inflation.

Business Overhead Expense

Determining with an advisor if Business Overhead Expense (BOE) disability insurance is warranted to protect the greatest asset of all—the practice itself—is important. BOE insurance could be vital for a solo practitioner or small practice in which associates would be lost without the owner. This insurance helps keep the lights on (ie, covers the rent or mortgage, all nonveterinary team member salaries, payroll taxes, utilities, maintenance costs) if the owner becomes disabled. Optionally, all or part of a replacement salary would be paid to a skilled, full-time, temporary veterinarian. The goal would be to keep the practice operational and revenues steady until the owner decides to return or until he or she is able to sell the practice at fair market value.

Unfortunately, few practice owners know about BOE. If a practice owner without BOE is faced with a disability, clients may leave when they cannot be seen and team members will worry about their next paycheck and may also leave. If the practice is put up for sale, the market will likely smell desperation and a low offer will result. In the author’s opinion, the protection BOE provides is not expensive relative to what is at stake.

Figure 2 Accidents unfortunately keep most people out of work for much more than a month—the average disability absence is approximately 2.5 years. Source: Council for Disability Awareness

Types of Disability Insurance Policies4

The 3 main disability insurance policy types are Group, Association, and Private. Each has advantages and disadvantages.

Group insurance is offered and paid for by employers. The benefits generally replace up to 60% of income and are taxable, netting 40% to 45% of original income.

Advantages: Employees do not pay for these policies, and these are not medically underwritten, so people with uninsurable, preexisting conditions can secure some income protection.

Disadvantages: Group policies are often not portable (ie, unavailable to anyone who leaves the practice) and commonly not occupation-specific at all or for a limited time only. Many group policies cap available benefits, so increasing incomes may outgrow the policy. Benefits for partial or residual disabilities are often limited.

Association policies are typically offered to students as they are leaving school—often with no medical underwriting, or later, with underwriting.

Advantages: Association policies may cost less and sometimes include additional riders, with no medical underwriting for veterinary students.

Disadvantages: Like Group policies, the benefits available may be capped. They may exclude coverage under certain conditions such as pregnancy, limit benefits for partial disabilities, or impose certain, less likely conditions that must be met before they will pay. They do limit occupation-specific benefits, and these policies can be quoted many different ways, making it extremely difficult to compare prices to other options. For example, the benefit amount may seem equal to another policy, but the ability to purchase future protection as income increases is limited, or important riders could be missing or unavailable, making it next to impossible for an untrained person to make comparisons.

Private disability insurance for someone who is insurable can often be a more suitable option, and pricing can be competitive with association policies. Insurability is determined by 3 factors—occupational, medical, and financial.

Advantages: Private policies replace up to 70% of income, can be occupation-specific throughout the entire policy, and commonly offer larger income replacement amounts and additional customized features. Premiums cannot be marked up or down; the prices are set by each state.

Disadvantages: Because policies are medically underwritten, medical conditions (eg, a back injury) may be excluded from coverage, limited to reduced benefits, or declined. Some private policies are far better than others, but like association policies, they can be difficult to compare because they can be quoted with small changes to fine details.

Note that all disability insurance is subject to fees, expenses, and restrictions.

Tax Considerations

Beware of deducting premiums on a tax return. The IRS disallows deducting the premiums for a policy and then receiving a tax-free benefit, so it is crucial to choose one or the other, which accountants are not always aware of. Not claiming premiums as a deduction for personal policies is recommended because the tax on premiums is less than the tax on benefits.

Employers pay group premiums, so they deduct those as business expenses and benefits are then taxable. A practice can pay premiums on the owner’s behalf if the practice is set up as an LLC or S-Corp, yet those premiums should be included in the owner’s salary. BOE policies pay for costs that are tax deductions themselves, so it is prudent and accepted to deduct BOE premiums as business expenses. Always consult a tax advisor for tax deduction rules.

Finding a Professional

Locating an independent, experienced financial professional who specializes in complex disability insurance can be challenging. Here are some resources that will help.

Go to the State Insurance Commissioner website or search Insurance Agent Look-Up to find a licensed, trained professional in your state.

Use brokercheck.finra.org to find information on a specific advisor.

Request to speak to the National Disability Insurance consultant through northstarfinancial.com/contact.

Using an independent advisor is critical. Multiple resources will provide a sense of the advisor’s affiliations and whether he or she has a strong obligation to place business with a specific company. An advisor who can give quotes from multiple companies does not necessarily have a track record of offering products outside the company’s proprietary products.

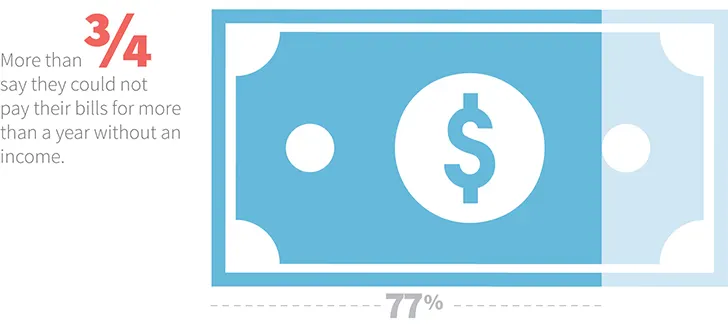

Figure 3 A majority of professionals have neither disability insurance nor enough savings to cover extended loss of income. Source: Council for Disability Awareness

Cost

Veterinarians sometimes object because of cost, yet disability insurance generally only costs between 1% to 3% of income.3

Conclusion

Most veterinarians rely on their income and cannot afford to be underinsured. Prudent financial preparation includes managing real threats and risks, and following the same advice veterinarians give their own clients—to protect their pets—makes wise sense.